U.S. Stocks Rally 10.4% in April

U.S. stocks rose 10.4% in April. The rally was triggered by the March 30th announcement that the U.S. would not invade Iran nor try to obliterate it. Relieved, investors began to buy back stocks and this buying has created its own momentum like in April 2025. The problem is that unlike last year with tariffs, the threat hasn’t really gone away and oil prices (futures) continue to price in a longer conflict. The 30-year Treasury Bond briefly hit 5%. Rising interest rates, rising oil prices and a sustained stock bull market are NOT mutually compatible. I don’t know how or when or from what level this ends (it could be much higher if we have mania tied to the IPOs of SpaceX and a couple major AI players), but I don’t think this year will end with the same 20%-ish gains as the past three years.

Earnings Growth — Strong but Accounting-Driven

Earnings growth has been very strong in the first quarter of 2026. That said, it is important to note that much of the growth is accounting-driven. The OBBBA or One Beautiful Bill accelerates write-offs among other things, as opposed to growth driven by demand volume. First quarter GDP was just reported at a fairly modest 2.0%.

(Learn more through our services: Third Party Assessment Management)

Domestic-to-Foreign Allocation Shift

In January I felt that a domestic-to-foreign stock ratio of 69%:31% was appropriate, noting that the dollar was trending weak, foreign markets were less expensive, and capital expenditures were really set to rise in developed markets ex-US. Today, because of the Iran situation and the indefinite blocking of the Straits of Hormuz, I would be more like 72%:28%. There is no getting around the fact that the present situation with respect to the cost of oil is more painful ex-US than it is here. The flip side of this is that if you asked me where I thought I’d be five years from now, I’d have probably said somewhere around 65%-67% US whereas now I’d say 62%-64% U.S. The developed world plus EM Asia will not forget that the U.S. in 2026 made decisions that only favored itself and Israel. (Read also: Our March 2026 Update)

Interest Rates — 30-Year Bond at 5%

It is significant that the 30-year bond is flirting with 5%. It will be even more significant if the 10 years breaches 4.5% and stays above it.

Notable Reads This Month

From Main Street Alpha “We are transitioning from a globalist, low-inflation environment, where tech multiples could expand to the moon on the back of zero-interest-rate policy to a nationalist, high-nominal growth era. If the regime is shifting toward nominal growth and persistent inflation, the biggest winners won’t be the innovators. The biggest winners will be… the monopolistic.”

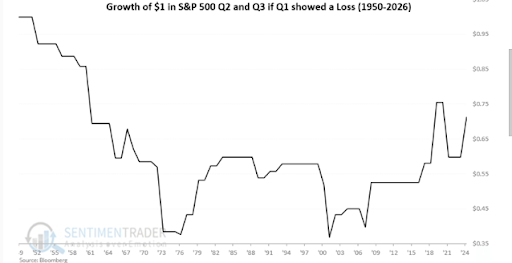

From Sentimentrader: Since 1950, the stock market has shown a collective loss in the middle of the year (April 1-September 30), though it has improved lately

From Howard Marks (Oaktree) on the value of being consistently above average: “I had dinner with the CIO of a pension fund. He explained that in his 14 years on the job, his fund had never been above the 27th percentile or below the 47th percentile. It was solidly in the second quartile of pension funds. As a result, for 14 years, he was in the fourth percentile”.

From Roy Amara on why new technologies are often priced wrong: “people tend to overestimate the short-term impact of new technologies while underestimating their long-term effects.”

From Ford CEO Jim Farley via Cedar Owl: “We cannot fill 5,000 mechanic jobs even at $120,000 per year”. This is not a wage problem. It is a structural training and cultural problem that cannot be solved by tariffs or subsidies.

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.